Yahoo News

Yahoo News Is Akebia Therapeutics (NASDAQ:AKBA) Using Debt Sensibly?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Akebia Therapeutics, Inc. (NASDAQ:AKBA) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Akebia Therapeutics

What Is Akebia Therapeutics's Debt?

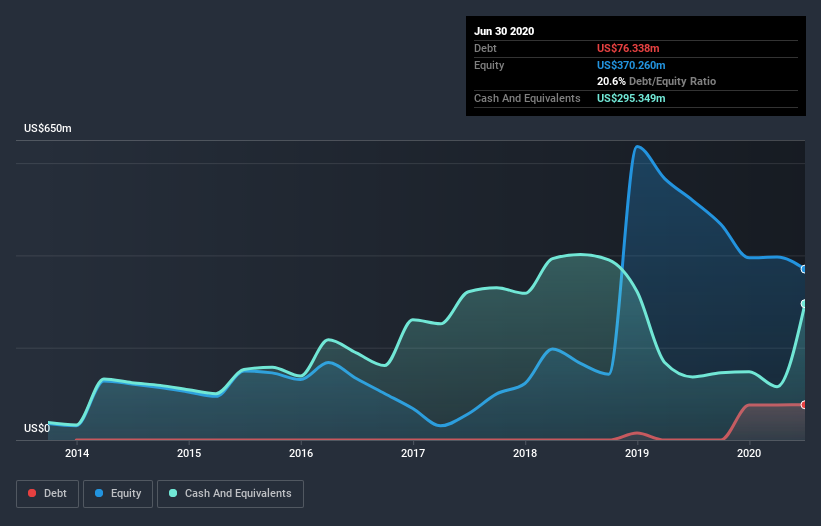

As you can see below, at the end of June 2020, Akebia Therapeutics had US$76.3m of debt, up from none a year ago. Click the image for more detail. But on the other hand it also has US$295.3m in cash, leading to a US$219.0m net cash position.

How Healthy Is Akebia Therapeutics's Balance Sheet?

The latest balance sheet data shows that Akebia Therapeutics had liabilities of US$195.8m due within a year, and liabilities of US$179.1m falling due after that. On the other hand, it had cash of US$295.3m and US$39.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$40.5m.

Of course, Akebia Therapeutics has a market capitalization of US$355.4m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Akebia Therapeutics boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Akebia Therapeutics can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Akebia Therapeutics wasn't profitable at an EBIT level, but managed to grow its revenue by 19%, to US$340m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Akebia Therapeutics?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Akebia Therapeutics lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$136m of cash and made a loss of US$386m. With only US$219.0m on the balance sheet, it would appear that its going to need to raise capital again soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 3 warning signs we've spotted with Akebia Therapeutics .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.