Yahoo News

Yahoo News These Analysts Just Made A Meaningful Downgrade To Their Mobvista Inc. (HKG:1860) EPS Forecasts

Market forces rained on the parade of Mobvista Inc. (HKG:1860) shareholders today, when the analysts downgraded their forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously. At US$3.74, shares are up 4.2% in the past 7 days. We'd be curious to see if the downgrade is enough to reverse investor sentiment on the business.

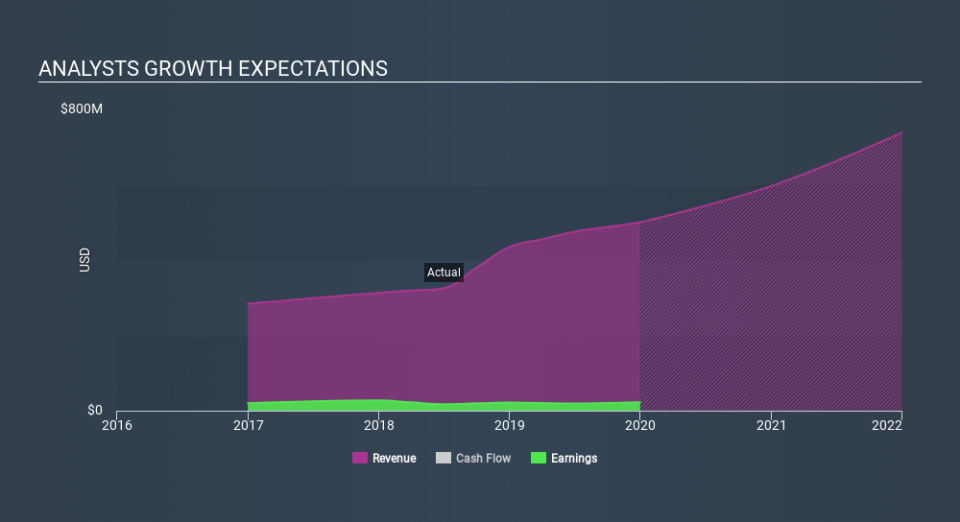

After this downgrade, Mobvista's dual analysts are now forecasting revenues of US$597m in 2020. This would be a meaningful 19% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to leap 107% to US$0.031. Prior to this update, the analysts had been forecasting revenues of US$677m and earnings per share (EPS) of US$0.041 in 2020. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a pretty serious decline to earnings per share numbers as well.

Check out our latest analysis for Mobvista

Analysts made no major changes to their price target of US$0.68, suggesting the downgrades are not expected to have a long-term impact on Mobvista'svaluation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. Next year brings more of the same, according to the analysts, with revenue forecast to grow 19%, in line with its 22% annual growth over the past three years. Compare this with the wider industry, which analyst estimates (in aggregate) suggest will see revenues grow 13% next year. So although Mobvista is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Mobvista.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have analyst estimates for Mobvista going out as far as 2021, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.