Yahoo News

Yahoo News Analysts Just Made A Notable Upgrade To Their Bird Construction Inc. (TSE:BDT) Forecasts

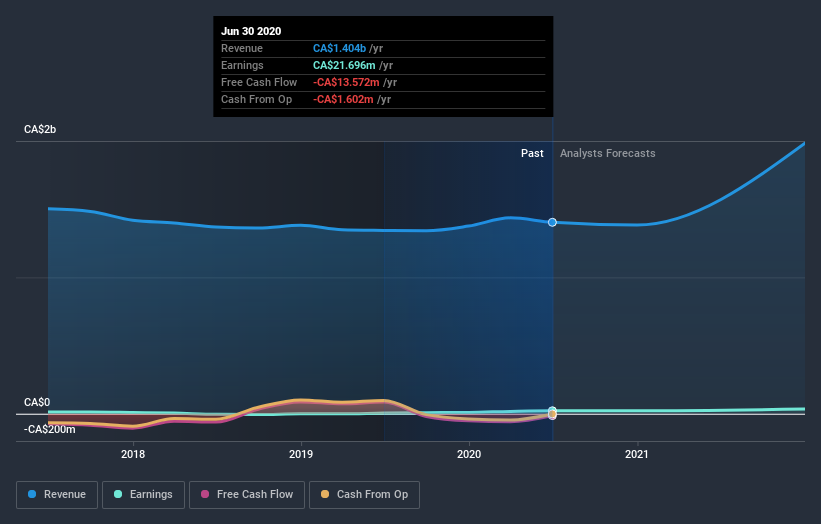

Bird Construction Inc. (TSE:BDT) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects.

After the upgrade, the two analysts covering Bird Construction are now predicting revenues of CA$1.5b in 2020. If met, this would reflect a credible 7.8% improvement in sales compared to the last 12 months. Per-share earnings are expected to increase 3.9% to CA$0.53. Prior to this update, the analysts had been forecasting revenues of CA$1.3b and earnings per share (EPS) of CA$0.41 in 2020. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

View our latest analysis for Bird Construction

Despite these upgrades, the analysts have not made any major changes to their price target of CA$9.88, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Bird Construction analyst has a price target of CA$11.00 per share, while the most pessimistic values it at CA$9.00. This is a very narrow spread of estimates, implying either that Bird Construction is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Of course, another way to look at these forecasts is to place them into context against the industry itself. For example, we noticed that Bird Construction's rate of growth is expected to accelerate meaningfully, with revenues forecast to grow 7.8%, well above its historical decline of 2.0% a year over the past five years. Compare this against analyst estimates for the wider industry, which suggest that (in aggregate) industry revenues are expected to grow 2.0% next year. So it looks like Bird Construction is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. The lack of change in the price target is puzzling, but with a serious upgrade to this year's earnings expectations, it might be time to take another look at Bird Construction.

Analysts are clearly in love with Bird Construction at the moment, but before diving in - you should be aware that we've identified some warning flags with the business, such as concerns around earnings quality. For more information, you can click through to our platform to learn more about this and the 2 other warning signs we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.