Yahoo News

Yahoo News How Does Progress Software's (NASDAQ:PRGS) CEO Pay Compare With Company Performance?

Yogesh Gupta became the CEO of Progress Software Corporation (NASDAQ:PRGS) in 2016, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

View our latest analysis for Progress Software

How Does Total Compensation For Yogesh Gupta Compare With Other Companies In The Industry?

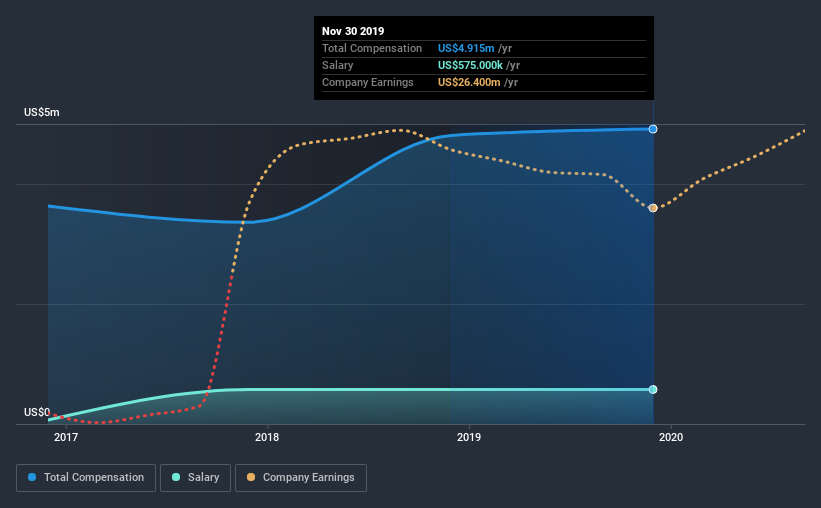

Our data indicates that Progress Software Corporation has a market capitalization of US$1.7b, and total annual CEO compensation was reported as US$4.9m for the year to November 2019. This means that the compensation hasn't changed much from last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$575k.

On comparing similar companies from the same industry with market caps ranging from US$1.0b to US$3.2b, we found that the median CEO total compensation was US$5.1m. So it looks like Progress Software compensates Yogesh Gupta in line with the median for the industry. Moreover, Yogesh Gupta also holds US$3.8m worth of Progress Software stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2019 | 2018 | Proportion (2019) |

Salary | US$575k | US$575k | 12% |

Other | US$4.3m | US$4.2m | 88% |

Total Compensation | US$4.9m | US$4.8m | 100% |

Talking in terms of the industry, salary represented approximately 13% of total compensation out of all the companies we analyzed, while other remuneration made up 87% of the pie. Although there is a difference in how total compensation is set, Progress Software more or less reflects the market in terms of setting the salary. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Progress Software Corporation's Growth Numbers

Over the past three years, Progress Software Corporation has seen its earnings per share (EPS) grow by 29% per year. Its revenue is up 11% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Progress Software Corporation Been A Good Investment?

With a three year total loss of 7.8% for the shareholders, Progress Software Corporation would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

In Summary...

As we noted earlier, Progress Software pays its CEO in line with similar-sized companies belonging to the same industry. On the other hand, the company has logged negative shareholder returns over the previous three years. However, EPS growth is positive over the same time frame. Considering positive EPS growth, we'd say compensation is fair, but shareholders may be wary of a bump in pay before the company logs positive returns.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 4 warning signs for Progress Software that you should be aware of before investing.

Important note: Progress Software is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.