Time to wrap-up here. European markets have dropped hard, and with the threat of further lockdowns hovering, it looks unlikely that the mood will improve quickly. These were some of the day’s top stories:

Stocks slide: Global markets have entered a sharp sell-off as fears grow that governments will introduce new lockdown measure in response to rising Covid-19 cases.

Watchdog finds potential breaches by KPMG in Carillion audit: The accounting watchdog has delivered a long-awaited report setting out possible breaches of professional standards by KPMG in its audit of collapsed government contractor Carillion.

Superdry makes sustainable fashion push: Superdry’s boss wants the fashion chain to be the world's “number one listed sustainable brand” despite slumping to a hefty annual loss.

Thanks for following along today. We’ll be back tomorrow morning!

03:10 PM

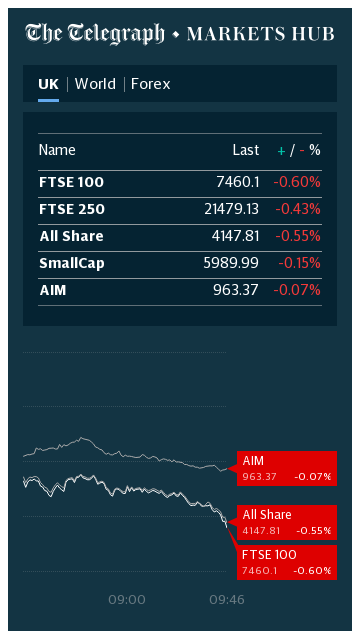

Market moves

As we near the European close, here’s how markets have moved today:

02:31 PM

DAX extends losses to 4.5pc

Germany’s DAX has extended its losses further even since my last post, dropping 4.5pc in its worst performance since March 27th. Deutsche Bank shares are down about 7.3pc currently.

02:25 PM

FTSE extends losses

The FTSE 100 has extended its losses once again, nearing the day’s lows once more. By my estimates, about £53bn has been wiped off the value of London’s blue-chips today.

Bloomberg TV - Bloomberg TV

02:13 PM

Lord Mayor’s Show scrapped due to pandemic

William Russell - Ollie Millington/Getty Images

The Lord Mayor’s Show, the long-running event which features a three-mile-long parade through the City of London, has been scrapped due to pandemic fears.

The annual event had been set to take place on November 14th as “contained, televised spectacle with no public access”.

The last time the show was cancelled was in 1952, during a period of mourning for the Duke of Wellington.

Lord Mayor William Russell said:

The Lord Mayor’s Show is a unique event but, because of serious and increasing concerns about the COVID-19 pandemic over the coming months, we believe that cancelling it is the right decision.Safety must remain our ultimate priority.

02:03 PM

Perugia: mystery solved?

My colleague Nick Squires tweets:

President of #Perugia airport tells me #BorisJohnson ‘definitely’ did not come through here this month. Says original press release confused him with Tony Blair, who did #perugiagate

US stocks have opened in the red, with the benchmark S&P 500 falling to its lowest level since July.

Bloomberg TV - Bloomberg TV

01:11 PM

Microsoft plans to buy games giant Zenimax, owner of Bethesda

Just in: Microsoft has announced plans to acquire Zenimax Media, the owner of Bethesda Softworks – maker of video games including the Elder Scrolls series – for $7.5bn in cash,

Microsoft said the acquisition is expected to close out in the second half of its 2021 fiscal year. It will bring the tech giant’s total number of creative studio teams from 15 top 23.

Microsoft is paying $7.5 billion for Zenimax/Bethesda

Security outsourcer G4S – continuing to puff its feathers in response to a hostile takeover attempt by Canadian firm GardaWorld – said its revenues have been “resilient” so far this year, with trading remaining strong since the first half.

As a result, the Group’s underlying earnings which were in line with 2019 at the six months stage are now ahead of the prior year for the first eight months of 2020. Although the global economic outlook remains uncertain, the Group’s performance in the first eight months demonstrates the strength of the business.

Chief executive Ashley Almanza added:

G4S today is a focused global business delivering technology-enabled security solutions. The benefits of our strategy, strong execution and timely response to Covid-19 continue to be reflected in the Group’s results during 2020 with resilient revenue, earnings and cash flow.

12:41 PM

Money round-up

Here are some of the day’s top stories from the Telegraph Money team:

Downing Street: Johnson to chair Covid-19 crisis meeting tomorrow

Boris Johnson’s spokesperson James Slack has told reporters that the PM will convene crisis talks over Covid-19 tomorrow.

Mr Johnson, who did not appear alongside top medical officials Chris Whitty and Sir Patrick Vallance at a briefing this morning, with chair a Cobra meeting and then a Cabinet meeting, to decide on the the Government’s next steps in response to the pandemic.

He will speak to leaders of Scotland, Wales and Northern Ireland later today.

12:06 PM

Watchdog finds possible breaches in KPMG’s audit of Carillion

Carillion - REUTERS/Darren Staples/File Photo

The accounting watchdog has delivered a long-awaited report setting out possible breaches of professional standards by KPMG in its audit of collapsed government contractor Carillion.

My colleague Michael O’Dwyer reports:

The Financial Reporting Council (FRC) said it sent its initial investigation report to KPMG on Aug 28 following its investigation into the firm’s audit of Carillion’s accounts in 2014, 2015 and 2016, along with additional work during 2017.

The probe was opened in January 2018, two weeks after Carillion fell into liquidation, and would normally be completed within two years.

However, the watchdog said in January that it would miss its self-imposed deadline for delivering the initial report because of the size and complexity of the investigation.

If the FTSE 100 locks in today’s poor performance, it would be the worst one-day session since June – narrowly worse than July’s biggest fall. Here’s how the change looks:

It would also be the 16th time the FTSE 100 has fallen more than 3pc in a single session in 2020 – a tumultuous year by any standard.

11:43 AM

Taxpayer faces £12bn bill as ministers ditch franchising

Grant Schapps - Chris J Ratcliffe/Getty Images

Propping up Britain’s Covid-hit train network is to cost taxpayers up to £12bn as ministers confirmed plans to scrap franchising in the biggest shake-up of the railways for a quarter of a century.

My colleague Oliver Gill reports:

Grant Shapps, the transport secretary, announced an extension of the emergency bankrolling of services for up to 18 months.

Franchising will then be replaced with an outsourced or “concession” model, where companies are paid a fee to run services with the Treasury collecting fares.

The changes, first revealed by The Telegraph earlier this month, mean taxpayers are on the hook for continued low passenger numbers, marking a radical reversal of the privatisation of the rail network under the dying days of John Major’s government 25 years ago.

Here’s how European markets have shifted today, with the FTSE 100 as the worst performer for most of the session:

The drag from banks is probably the biggest factor in FTSE’s underperformance, although it has levelled off somewhat in recent minutes.

Shore Capital’s Gary Greenwood reckons there’s no good reason to for markets to punish lenders based on yesterday’s revelations:

While the details of the FinCEN files highlight potential wrongdoing by the banks over a number of years, including having continued to facilitate suspicious transactions beyond filing the original suspicious activities report (SAR), it is not clear to us that this news represents a fresh reason to punish the banks involved or whether this is something that the authorities will have previously dealt with as it was information they already knew about.

Investors, apparently, disagree.

Overall, it remains travel and hospitality stocks that are taking the heaviest hit:

Hospitality and travel stocks taking a battering as new restrictions loom:

Ah. Markets are blood-red across Europe in the biggest sell-off since July, and Wall Street is set to join the drop at the open in couple of hours’ time.

The dollar is strengthening amid a shift to low-risk assets, which is dragging down the pound slightly and offering some support to London’s blue-chips in the process.

Equities are caught in a one–two punch today: expectations of fresh lockdowns are in overdrive, and and banks are getting battered over yesterday’s report into their alleged failure to prevent the spread of dirty money.

11:12 AM

Handover

That's all from me for today – a busy morning for markets, to say the least.

My colleague Louis Ashworth will be taking over to steer you through all of the events this afternoon.

Thanks for following!

10:47 AM

Still falling...

London's blue-chip index has already fallen by 200 points this morning, or 3.5pc – the most since July.

The government's chief medical advisers have warned that the UK could face 50,000 new virus cases per day by mid-October without action.

The gloomy press conference (which did not include any questions from journalists) is likely to be a precursor for the government to impose new restrictions later this week.

10:26 AM

More on Rolls...

Rolls

Rolls-Royce shares have plummeted 8pc after the engineering giant confirmed it is considering tapping investors for £2.5bn to shore up its finances.

Shares in the business tumbled by as much as 10pc in early trading after it confirmed reports that the fundraiser was a funding option being reviewed by the business.

It told investors that, amongst other options, it is "evaluating" the merits of raising up to £2.5 billion in equity through a rights issue or other fundraiser.

The review will also see it consider taking on new debt to support its finances after the aerospace industry was hammered by the pandemic.

Last month, Rolls warned that its future could be at risk if the Covid downturn becomes even more severe, after plunging to a record £5.4bn half-year loss.

At the time, analysts at JP Morgan said: "Only a very major capital raise would put [Rolls] on a sound footing."

10:05 AM

Watch live: Chris Witty and Sir Patrick Vallance issue warning about second wave

You can watch the presentation from the Chief Medical Officer and Chief Scientific Adviser here:

09:51 AM

Did Boris travel to Perugia?

Markets are plunging and a second lockdown looms, but SW1 is gripped this morning with a story from La Republica that Boris Johnson went on a "mystery trip" to Italy last week.

No 10 has strongly denied the report but my colleague Cat Neilan says Tory MPs have their suspicions...

Downing Street is denying it - but backbenchers certainly believe @antoguerrera's excl, claiming the PM was in Perugia this month.

One tells me the background on his Zoom call with Tory MPs that Friday "definitely wasn't the normal room in No 10" https://t.co/26ncpQyNJd

Bank stocks are reeling this morning following accusations that they enabled the "flow of dirty money".

09:14 AM

Unilever’s Dutch investors approve single London HQ

Unilever HQ

Shareholders in the Dutch arm of Unilever voted in favor of unifying its headquarters in the UK, advancing a plan to streamline a cumbersome structure that has complicated major takeovers and disposals.

Bloomberg has the details:

The vote, announced at an extraordinary general meeting Monday, is a key step toward ending the Dove soap owner’s dual nationality. It will be followed by another ballot next month, polling shareholders in the British arm.

More than 99% of the Dutch arm’s investors approved the plan, Unilever said.

Approval from both sides would hand a win to Chief Executive Officer Alan Jope after the company withdrew a proposal to unify its business in the Netherlands under his predecessor, Paul Polman, in 2018. That reversal came after U.K. stockholders rebelled against the company’s potential exit from the FTSE 100 index.

08:49 AM

BBC: Full national lockdown is not an option, says No 10

The BBC's Laura Kuenssberg is reporting that the view from Downing Street is that a "full national lockdown not an option". However, they are set on implementing new restrictions to slow the spread of the virus.

View from No 10 - doing nothing is not an option, but full national lockdown not an option - decisions about precise options not finished despite hours of meetings yday

The blue-chip index is pushing deep into the red, and is now down 2.7pc.

British Airways owner IAG is the biggest faller, down 12pc, while Rolls Royce is trading almost 10pc lower following reports that the engine maker is looking to tap investors for £2.5bn.

European market - Bloomberg

08:24 AM

Sweden turns on spending taps to revive economy

Sweden

Sweden’s government will pump $12bn (£9.3bn) into the economy in 2021 through tax cuts and increased spending in an attempt to boost its virus-stricken economy.

The government forecast Sweden’s GDP will shrink by around 4.6pc this year in its budget on Monday, a smaller hit than many other European countries after applying a more light-touch approach to Covid-19 restrictions.

The coalition government said: "Together we are going to work Sweden’s way out of the crisis and build a more sustainable society."

While many countries in Europe are re-imposing restrictions after a spike in new cases, Sweden's infection rate remains low and its economy remains open.

Sweden's Social Democrat and Green coalition said the focus would be on boosting jobs, welfare and supporting the switch to a carbon-free future as it outlined a raft of tax cuts and new spending.

07:58 AM

FT: Sunak to extend coronavirus business loans

Sunak

The FT is reporting that Chancellor Rishi Sunak is to extend the Treasury’s UK-wide programme of business support loans as ministers threaten a second lockdown.

The FT says:

Mr Sunak is this week expected to unveil plans to extend four loan schemes, which have already backed £53bn in lending to companies through government guarantees, in a sign that new national support measures are needed to avert widespread business collapses and mass job losses.

The move to bolster businesses comes as the government weighs up whether to do more to counter the spread of Covid-19, including new national restrictions in England. Sadiq Khan, London mayor, on Sunday held talks with ministers on possible new restrictions in the capital.

Under plans being drawn up by the Treasury, the business loan schemes will all be extended for applications until the end of November, with banks allowed to process loans until the end of the year. The Treasury declined to comment.

Three of the programmes were due to end this month for applications. The fourth — the “bounce back” loan scheme — was scheduled to close at the start of November.

According to two people familiar with the talks, the extension is set to include the Future Fund — the innovative support programme that could see the government take stakes in scores of fast-growing start-ups forced to take state-backed convertible loans.

07:42 AM

HSBC shares plunge to 25-year low

Shares in HSBC slumped to a 25-year low, as pressures mounts on several fronts, including a potential threat to its China expansion plans and increased scrutiny of money laundering controls.

On Sunday, The Telegraph reported that HSBC and Standard Chartered are bracing for a renewed US sanctions assault on China, amid official concern that escalating diplomatic tensions threaten collateral damage in the City.

Over the weekend, the bank was also accused of allowing money from a Ponzi scheme to be transferred around the world, following a leak of secret files.

The bank’s Hong Kong shares on Monday slid below their closing low for March 2009, hitting as low as HK$29.60. They have plunged by half this year, reaching the lowest since 1995. In London, HSBC fell 3.8pc to 292.6p.

07:19 AM

Superdry losses almost double

Superdry

Clothing brand Superdry nearly doubled its losses in its most recent financial year as it dealt with the first month of lockdown.

PA has the details:

The retailer said that pre-tax loss reached £166.9m in the 12 months ending April 25, up 87pc from last year's £89.3m loss.

It came as Superdry was forced to close all of its stores in the last month of the financial year, pushing revenue down 19pc to £704.4m.

But the drop in revenue was also evidence of a change in direction for the business.

Since founder Julian Dunkerton returned to the fold in April last year he has started slashing discounts on its stores.

In January he said that the proportion of the business's sales that were discounted had halved over the peak trading period, around Christmas.

But it is a plan that Mr Dunkerton has been forced to - at least temporarily - shelve because of the Covid-19 pandemic.

"We have discounted more in recent months compared to the prior year to help clear excess stock which accumulated during the temporary store closures resulting from Covid-19," bosses said on Monday.

07:09 AM

Europe tumbles at the open

Red all over. European equities have opened in the red as fears grow that a resurgence in coronavirus cases across the continent will slow the economic recovery.

UK bank stocks are also under pressure after being accused of enabling fraudsters, criminals and money-launderers, following a leak of secret files over the weekend.

European market data - Bloomberg

06:46 AM

Government rolls over emerency measures for rail companies

Waterloo

Rail franchising has been "ended" by extending measures introduced to keep trains running after the coronavirus outbreak, the Department for Transport (DfT) has announced.

We report:

Operators have been moved to "transitional contracts" ahead of the creation of a "simpler and more effective structure" which will be developed over the coming months, the DfT said.

The department has taken on franchise holders' revenue and cost risks since March, at a cost to taxpayers of at least £3.5bn.

"Significant taxpayer support will still be needed" under the new Emergency Recovery Management Agreements, the DfT said.

Transport Secretary Grant Shapps said: "The model of privatisation adopted 25 years ago has seen significant rises in passenger numbers, but this pandemic has proven that it is no longer working.

"Our new deal for rail demands more for passengers. It will simplify people's journeys, ending the uncertainty and confusion about whether you are using the right ticket or the right train company.

Good morning. The FTSE 100 is set to open firmly in the red as fears of a second national UK lockdown mount.

FTSE futures are pointing down about 1.1pc after reports that Boris Johnson will threaten another country-wide shutdown if the public does not follow strict self-isolation and social distancing rules.

5 things to start your day

1) Truss to rip up rules on assessing trade deals: Liz Truss is ready to rip up the Trade Department’s rule books on assessing deals in an effort to improve how it measures the economic benefits of its post-Brexit “Global Britain” project.

2) UK banks enabled ‘flow of dirty money’, leaked secret files claim: A cache of more than 2,000 suspicious activity reports (SARs) – those filed to the authorities by banks who suspect wrongdoing – reportedly contains allegations that a number of major UK lenders allowed dirty money to flow through their accounts.

4) Manufacturers scale back plans for investment in wake of Covid: Manufacturers are slashing investment as they fight to survive the impact of coronavirus and growing Brexit worries, echoing the collapse seen in the wake of the great financial crisis.

5) Dropping demand forces consultants to slash fees by 30pc: Consultants are being forced to cut their fees by up to 30pc as demand drops and a pause in on site working during the pandemic allows more firms to compete for contracts regardless of their location.

What happened overnight

Asian shares and most currencies held tight ranges on Monday, as investors awaited developments on US fiscal stimulus and coronavirus vaccines amid a resurgence of infections in Europe.

MSCI's broadest index of Asia-Pacific shares outside Japan was 0.1pc weaker, though it was not too far from a June 2018 peak at 568.84.

Australia's benchmark index slipped 0.5pc while New Zealand's stumbled 0.6pc. Chinese shares opened in the red with the blue-chip index down 0.3pc.

Japanese markets were closed for a public holiday.

The dollar slipped 0.1pc against a basket of major currencies to 92.855.

Against the safe haven yen, the greenback eased 0.2pc to 104.35 to drift closer to a recent 3.5-month trough.

The euro was up 0.25pc at $1.2946 while the risk-sensitive Australian dollar was also slightly higher at $0.7304. The British pound was up 0.25pc at $1.2947.

The Money Saving Expert has issued a warning to UK homeowners who have curtains hanging up in their homes - saying you could save hundreds by following his advice.

Motorists can save up to 25 percent on petrol and diesel by removing one item from their car, according to motoring experts. The item in question is a common sight on many vehicles

Gemma Atkinson has spoken about her relationship with her fiance Gorka Marquez, including having discussed them being away from each other due to work commitments.

Prince Harry and his brother Prince William were said to be inseparable - but one moment six years ago at Harry's wedding their 'happiness together' reportedly changed

BBC Question Time host Fiona Bruce was forced to intervene and reprimand a Tory Cabinet Secretary after he launched a personal attack on another panellist ...

Israel’s presumed counterstrike against Iran has proved Joe Biden and David Cameron wrong in their insistence that Israel should just “take the win”. Instead, it fought back – and yesterday Iran was trying to pretend that nothing had happened.

Israel’s strike on Iran on Friday morning will not come as a surprise to Western observers – but it will cause great concern in Washington and London as the region tips closer towards an all-out war.

If this Israeli attack on Iran is no more than it presently appears to be, then it is rather well modulated. If the airbase at Isfahan has been attacked - home to the 8th Tactical Air Wing of the Iranian Air Force, and not a Revolutionary Guard installation - then the Israelis are making their point against a conventional military target. It is not an enrichment plant or a reactor, but the wide-ranging nuclear research conducted there involves some 3,000 Iranian nuclear scientists.

Yahoo News

Yahoo News