Yahoo News

Yahoo News How Is Prophecy International Holdings' (ASX:PRO) CEO Paid Relative To Peers?

Brad Thomas has been the CEO of Prophecy International Holdings Limited (ASX:PRO) since 2016, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Prophecy International Holdings.

View our latest analysis for Prophecy International Holdings

Comparing Prophecy International Holdings Limited's CEO Compensation With the industry

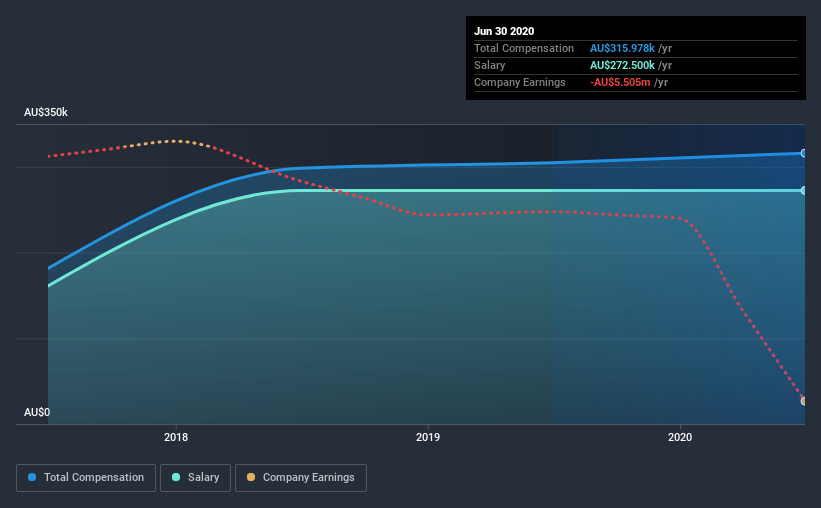

At the time of writing, our data shows that Prophecy International Holdings Limited has a market capitalization of AU$38m, and reported total annual CEO compensation of AU$316k for the year to June 2020. That's a fairly small increase of 3.7% over the previous year. We note that the salary portion, which stands at AU$272.5k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations under AU$282m, the reported median total CEO compensation was AU$340k. This suggests that Prophecy International Holdings remunerates its CEO largely in line with the industry average.

Component | 2020 | 2019 | Proportion (2020) |

Salary | AU$273k | AU$273k | 86% |

Other | AU$43k | AU$32k | 14% |

Total Compensation | AU$316k | AU$305k | 100% |

Speaking on an industry level, nearly 60% of total compensation represents salary, while the remainder of 40% is other remuneration. Prophecy International Holdings is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Prophecy International Holdings Limited's Growth Numbers

Over the last three years, Prophecy International Holdings Limited has shrunk its earnings per share by 86% per year. Its revenue is up 13% over the last year.

Few shareholders would be pleased to read that EPS have declined. And while it's good to see some good revenue growth recently, the growth isn't really fast enough for us to put aside my concerns around EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Prophecy International Holdings Limited Been A Good Investment?

Prophecy International Holdings Limited has served shareholders reasonably well, with a total return of 18% over three years. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

As we touched on above, Prophecy International Holdings Limited is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. Prophecy International Holdings has had a poor showing when it comes to EPS growth, and it's tough to say that shareholder returns have done much to excite us. These figures do not go well against CEO compensation, which is more or less equal to the industry median. Considering all of this, we can't say the CEO is underpaid, and moving forward shareholders will likely want to see higher growth to justify any raise.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 2 warning signs for Prophecy International Holdings you should be aware of, and 1 of them doesn't sit too well with us.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.