Yahoo News

Yahoo News

Traders are starting to question whether the US dollar will continue to rally

Massimo Bettiol/Getty

Currency speculators sold the US dollar ahead of last Friday’s US non-farm payrolls report.

Traders are still long commodity currencies, but are betting against the Japanese yen and Swiss franc.

This weeks US FOMC interest rate decision and CPI report will likely determine whether US dollar selling will persist.

Currency traders, as a whole, still expect the US dollar to strengthen in the period ahead. However, confidence in that view appears to be slipping.

That’s the finding of the latest Commitment of Traders (CoT) report released by the US Commodity Futures Trading Commission (CFTC) last Friday, with net long US dollar positioning in the greenback falling for a third consecutive week.

“Leveraged funds marginally pared back their net long USD position ahead of the US non-farm payrolls data,” said Khoon Goh and Rini Sen, FX Strategists at ANZ Bank. “Funds reduced their long USD exposure by $300 million to $7.3 billion, the third consecutive week where positions were reduced.”

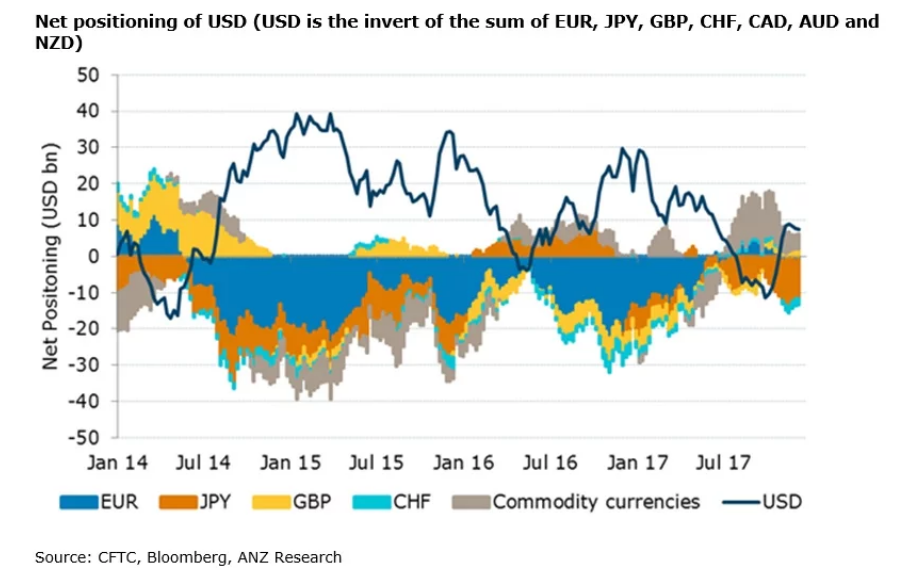

Net speculative positioning, defined as non-commercial positions reported by the CFTC, is the sum of long and short options and futures positions in a particular asset, in this case the US dollar.

A net long position indicates that traders, collectively, are looking for strength ahead.

This chart from ANZ shows net US dollar speculative positioning in the US dollar against other G10 currencies.

Source: ANZ

According to the pair, the dollar was sold against all major currencies aside from the Japanese yen and Australian dollar during the week.

“Funds added to their overall net short JPY position by $300 million to $10.7 billion, reversing the net buying from the previous two weeks,” Goh and Sen said.

“Net AUD longs were trimmed for the ninth consecutive week, by $200 million to $3.4 billion.”

However, net buying was recorded in the European currencies such as the euro, UK pound and Swiss Franc, along with the Canadian and New Zealand dollars.

“Net EUR shorts were reduced by $300 million to $800 million even as the ECB is expected to spring no surprises at its last policy meeting of the year,” the pair said.

“Net GBP longs were further raised by $200 million to $2.2 billion, the fourth consecutive week of net buying.”

Net shorts in the Swiss franc and New Zealand dollar were also trimmed modestly, while net buying in the Canadian dollar also increased.

While the CoT report only captures positioning reported by the CFTC, not the entire market, it can be used to extrapolate broader views held by currency traders.

Goh and Sen say that there’s likely to be further positioning changes ahead of this week’s US CPI data and the FOMC meeting where a 25 basis point rate hike is fully priced by market.

The US Federal Reserve’s December FOMC rate decision, including updated economic forecasts, will be released at 6am AEDT on Thursday, December 14, just over five hours after separate data on US consumer price inflation (CPI) for November.

NOW WATCH: A Navy SEAL explains what to do if you're attacked by a dog

See Also: