Yahoo News

Yahoo News UniFirst Corporation Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

UniFirst Corporation (NYSE:UNF) came out with its quarterly results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. Results were mixed, with revenues of US$446m exceeding expectations, even as earnings per share (EPS) came up short. Statutory earnings were US$1.12 per share, -10% below whatthe analysts had forecast. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for UniFirst

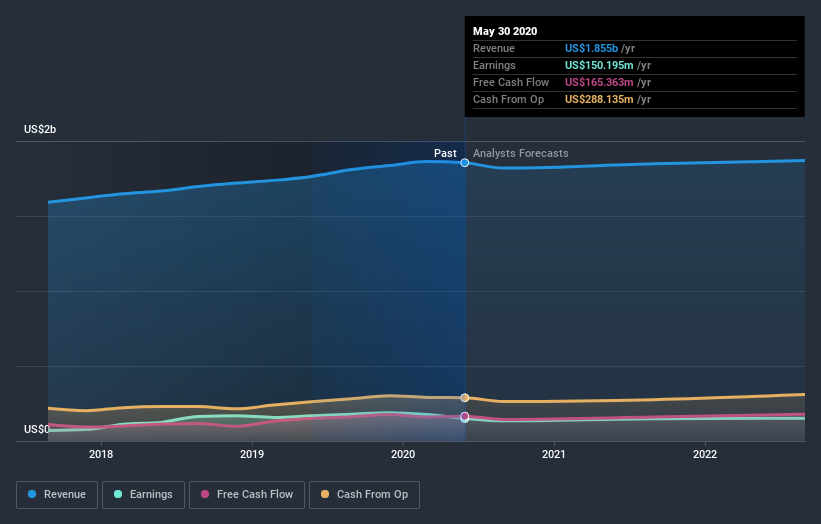

Following last week's earnings report, UniFirst's four analysts are forecasting 2021 revenues to be US$1.85b, approximately in line with the last 12 months. Statutory per-share earnings are expected to be US$7.86, roughly flat on the last 12 months. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.77b and earnings per share (EPS) of US$7.66 in 2021. So there seems to have been a moderate uplift in sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

It will come as no surprise to learn that the analysts have increased their price target for UniFirst 11% to US$196 on the back of these upgrades. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on UniFirst, with the most bullish analyst valuing it at US$206 and the most bearish at US$185 per share. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that sales are expected to reverse, with the forecast 0.3% revenue decline a notable change from historical growth of 5.8% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.5% annually for the foreseeable future. It's pretty clear that UniFirst's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards UniFirst following these results. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on UniFirst. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple UniFirst analysts - going out to 2022, and you can see them free on our platform here.

We also provide an overview of the UniFirst Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.