Yahoo News

Yahoo News United Airlines Holdings, Inc. Full-Year Results: Here's What Analysts Are Forecasting For Next Year

United Airlines Holdings, Inc. (NASDAQ:UAL) shares fell 5.2% to US$84.88 in the week since its latest full-year results. Results were roughly in line with estimates, with revenues of US$43b and statutory earnings per share of US$11.58. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether analysts have changed their mind on United Airlines Holdings after the latest results.

Check out our latest analysis for United Airlines Holdings

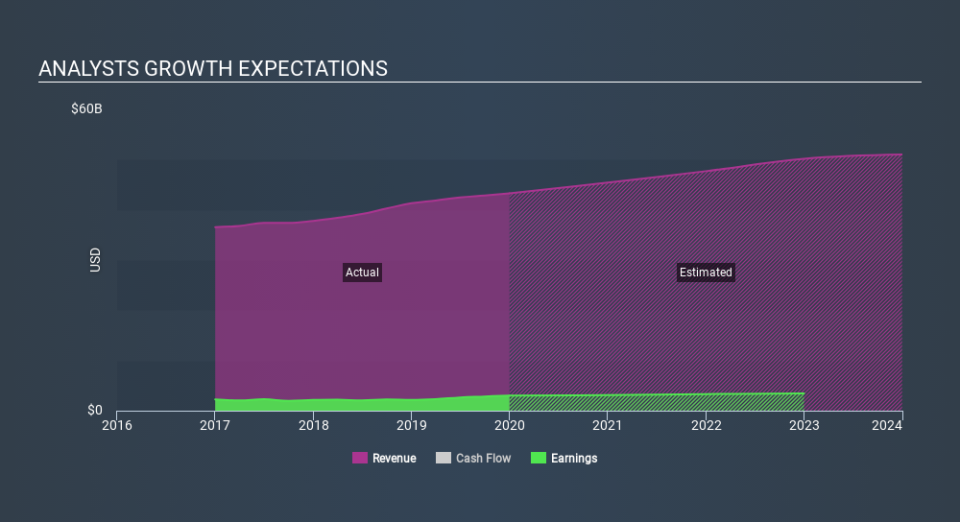

Taking into account the latest results, the latest consensus from United Airlines Holdings's 16 analysts is for revenues of US$45.4b in 2020, which would reflect a modest 5.0% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to accumulate 7.9% to US$12.50. Before this earnings report, analysts had been forecasting revenues of US$45.6b and earnings per share (EPS) of US$12.58 in 2020. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

It will come as no surprise then, to learn that the consensus price target is largely unchanged at US$108. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values United Airlines Holdings at US$140 per share, while the most bearish prices it at US$90.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. Analysts are definitely expecting United Airlines Holdings's growth to accelerate, with the forecast 5.0% growth ranking favourably alongside historical growth of 2.5% per annum over the past five years. Compare this with other companies in the same market, which are forecast to grow their revenue 5.1% next year. United Airlines Holdings is expected to grow at about the same rate as its market, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most obvious conclusion from these results is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider market. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on United Airlines Holdings. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple United Airlines Holdings analysts - going out to 2023, and you can see them free on our platform here.

You can also view our analysis of United Airlines Holdings's balance sheet, and whether we think United Airlines Holdings is carrying too much debt, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.