Yahoo News

Yahoo News Is Venator Materials (NYSE:VNTR) A Future Multi-bagger?

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So when we looked at Venator Materials (NYSE:VNTR) and its trend of ROCE, we really liked what we saw.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Venator Materials:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

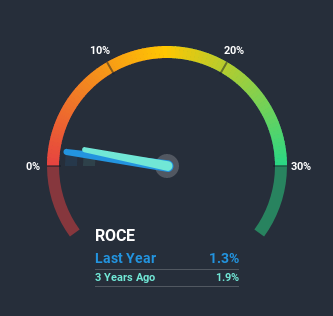

0.013 = US$26m ÷ (US$2.3b - US$371m) (Based on the trailing twelve months to June 2020).

Therefore, Venator Materials has an ROCE of 1.3%. In absolute terms, that's a low return and it also under-performs the Chemicals industry average of 9.6%.

View our latest analysis for Venator Materials

Above you can see how the current ROCE for Venator Materials compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Does the ROCE Trend For Venator Materials Tell Us?

We're delighted to see that Venator Materials is reaping rewards from its investments and has now broken into profitability. The company now earns 1.3% on its capital, because four years ago it was incurring losses. On top of that, what's interesting is that the amount of capital being employed has remained steady, so the business hasn't needed to put any additional money to work to generate these higher returns. With no noticeable increase in capital employed, it's worth knowing what the company plans on doing going forward in regards to reinvesting and growing the business. After all, a company can only become a long term multi-bagger if it continually reinvests in itself at high rates of return.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 16%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

What We Can Learn From Venator Materials' ROCE

To sum it up, Venator Materials is collecting higher returns from the same amount of capital, and that's impressive. And since the stock has dived 90% over the last three years, there may be other factors affecting the company's prospects. Still, it's worth doing some further research to see if the trends will continue into the future.

If you'd like to know about the risks facing Venator Materials, we've discovered 1 warning sign that you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.