Yahoo News

Yahoo News Why Investors Shouldn't Be Surprised By Carriage Services, Inc.'s (NYSE:CSV) P/E

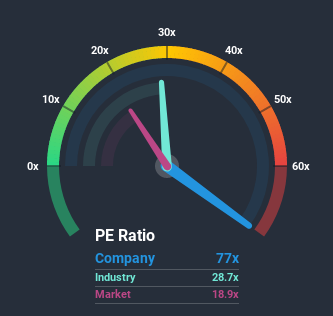

With a price-to-earnings (or "P/E") ratio of 77x Carriage Services, Inc. (NYSE:CSV) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 10x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Carriage Services has been struggling lately as its earnings have declined faster than most other companies. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

See our latest analysis for Carriage Services

Want the full picture on analyst estimates for the company? Then our free report on Carriage Services will help you uncover what's on the horizon.

Is There Enough Growth For Carriage Services?

The only time you'd be truly comfortable seeing a P/E as steep as Carriage Services' is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 49% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 77% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 444% over the next year. With the market only predicted to deliver 3.2%, the company is positioned for a stronger earnings result.

With this information, we can see why Carriage Services is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Carriage Services' P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Carriage Services' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 4 warning signs for Carriage Services (of which 1 can't be ignored!) you should know about.

You might be able to find a better investment than Carriage Services. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a P/E below 20x (but have proven they can grow earnings).

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.