Yahoo News

Yahoo News These 4 Measures Indicate That TrueBlue (NYSE:TBI) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, TrueBlue, Inc. (NYSE:TBI) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for TrueBlue

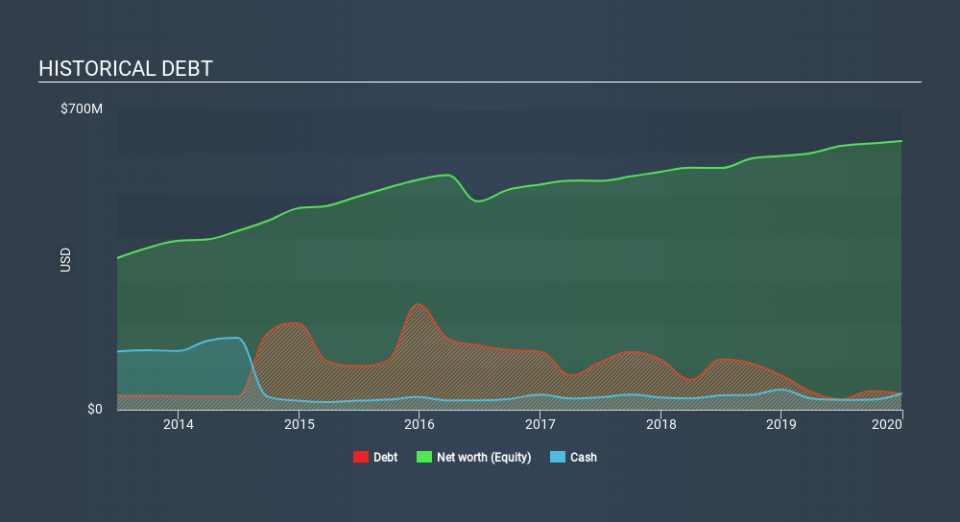

What Is TrueBlue's Net Debt?

As you can see below, TrueBlue had US$37.1m of debt at December 2019, down from US$80.0m a year prior. But it also has US$37.6m in cash to offset that, meaning it has US$508.0k net cash.

How Strong Is TrueBlue's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that TrueBlue had liabilities of US$230.8m due within 12 months and liabilities of US$279.4m due beyond that. On the other hand, it had cash of US$37.6m and US$353.4m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$119.2m.

This deficit isn't so bad because TrueBlue is worth US$475.8m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, TrueBlue also has more cash than debt, so we're pretty confident it can manage its debt safely.

On the other hand, TrueBlue's EBIT dived 16%, over the last year. If that rate of decline in earnings continues, the company could find itself in a tight spot. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine TrueBlue's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. TrueBlue may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, TrueBlue actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

Although TrueBlue's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$508.0k. And it impressed us with free cash flow of US$65m, being 112% of its EBIT. So we don't have any problem with TrueBlue's use of debt. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that TrueBlue is showing 2 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.