Yahoo News

Yahoo News Interest Rates Have Gone Up – And These Graphs Show Just How Bad That Is

Why does it matter if interest rates go up or down? (Photo: sesame via Getty Images)

There’s some more bleak news for the UK economy after the Bank of England’slatest statement.

The Bank has just increased its base rate by the largest amount for 33 years, from 2.25% to 3%, while also predicting a two-year recession and a fall in inflation next year.

Here’s everything you need to know to understand what this is causing major concern.

What is an interest rate?

This is the cost of borrowing, and is seen as an indicator of how the economy is doing.

It’s also the means by which the Bank controls inflation.

Inflation is the rate at which the price of goods and services increase – and it’s currently at level not seen for 40 years, 10.1%. The Bank aims to have it at just 2%.

By increasing interest rates, the Bank can bring down inflation by reducing how much people spend.

The energy crisis, exacerbated by the war in Ukraine, and soaring food prices, have been the driving factors behind these leaps.

So interest rates affect the way people spend money, how much it costs to borrow money and how people save.

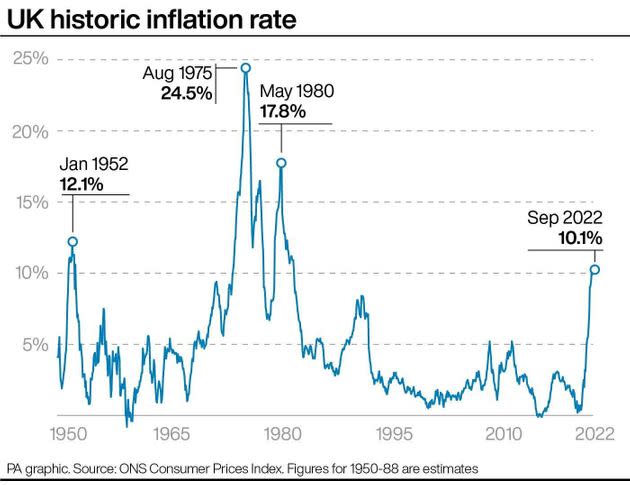

This graph shows how inflation is at a level not seen since the 1980s.

UK historic inflation rate. (Photo: PA Graphics via PA Graphics/Press Association Images)

So what does it mean if interest rates go up?

If interest rates go up, people tend to spend less.

Mortgage rates become more expensive, meaning homeowners will have to pay lenders more money each month.

Around 1.6 million people on tracker and variable deals will see an instant increase in their monthly payments, although those on fixed rate mortgages will not seen an instant change.

New buyers will have to pay more if they want to take out the same mortgage as they did compared to a year ago.

Credit cards, bank loans and car loans will also charge borrowers more.

Those with saving will actually benefit. Individual banks and building societies are offering a higher return on their money than usual – although interest rates are not keeping up with rising prices, so the value of UK money is falling.

What does it mean if interest rates go down?

Those with savings will earn less on their money, and it will cost less to borrow money.

That means it becomes an ideal time to take out a mortgage, a car loan, businesses might look to expand or take on more employees.

How high have interest rates been in the past?

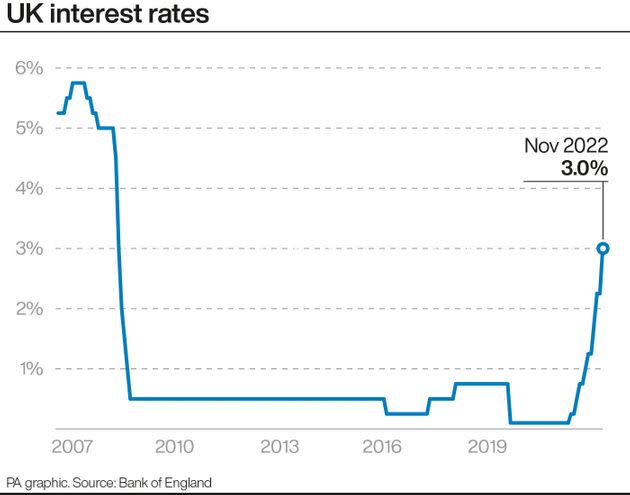

Interest rates in the UK were much higher before the financial crash of 2008.

This graph shows how the rates around 2007 hoovered between 5% and 6% in in interest rates, before being dramatically slashed to under 1% the following year.

Interest rates remained stable at 0.5% until 2016, when they dipped again slightly before rising again just under 1% up until 2019.

UK interest rates have soared to levels not seen since the 2008 financial crash (Photo: PA Graphics via PA Graphics/Press Association Images)

The pandemic saw interest rates drop to a historic low of 0.1% – then the Bank started to increase it at a rapid speed.

Now, in November 2022, it has reach 3% following eighth consecutive increases in the rate from the Bank.

This is the largest singular hike since 1989.

But, for context, historic interest rates were much higher.

They would fluctuate between 4 and 5% during the 18th Century, and by the 19th Century it was between 4 and 10%, according to financial website Mortgage Strategy.

Rates then fluctuated between 5 and 10% during the first half of the 20th Century.

In 1979, Margaret Thatcher increased it to a huge 17% to tackle inflation. It slowly ebbed down, and then rose again to 12% in September 1992, on Black Wednesday, before dropping to around 10% and gradually declining until closer to around 5%.

If it’s been so much higher in the past, why does it matter now?

As Sky News’ Ed Conway pointed out, interest rate expectations from the Bank of England have changed dramatically in recent months.

In August, they were expected to peak at 2.75%. In September, the expected peak was 4.75%. Now, the expected peak in 5.25%.

But, as Conway explained in a Twitter thread from September, it all depends on how affordable those rates are for mortgage holders.

“What matters is not just the RATE but how much you’re borrowing and (equally important) how high your disposable income is vs those payments,” he wrote.

He noted that when debt and stagnant wages are taking into the picture, it becomes very different.

Add all those things to the equation - debt burdens, incomes, mortgage terms and mortgage rates - you end up with a very different picture.

Here’s data from @resi_analyst who’s worked out the “equivalent” interest rate - eg the actual BURDEN of interest rates over time. pic.twitter.com/vWrTdGq6kK— Ed Conway (@EdConwaySky) September 22, 2022

So, how high will interest rates go?

The Bank of England previously warned that the rate will reach 5.25% by the third quarter of 2023 – although that would cripple growth.

Now, the analysts have suggested rates could reach the lower level of 4.75% next year, since the turmoil in the financial markets after the mini-budget has settled down.

And what does that mean for a recession?

So a recession is when there are two quarters of negative growth in the UK economy.

According to the Bank, the UK is going to enter the worst recession since reliable records began in 1920s, lasting for two years – although it is not expected to be as severe at the 2008 financial crash.

While the UK economy has struggled for a long period before, it’s been punctuated with short bursts of growth.

This means the gross domestic product (GDP) could shrink for every quarter, with growth only returning to the UK economy in the middle of 2024.

“If we don’t tackle the inflation [through interest rates], then the problem gets worse. That would rebound onto to both the duration and nature of the recession, I think,” Bank of England governor Andrew Bailey said on Thursday.

The trouble is, interest rates decreases spending – which should shrink the economy. So, as the Bank suggested, it’s likely future interest rate rises will be smaller.

This article originally appeared on HuffPost UK and has been updated.

Related...

What The Bank Of England's Historic Announcement Means For You

Tory Donor Warns Economy Is 'Doomed' And Conservatives Are Not 'Fit' To Run Country