Yahoo News

Yahoo News Jobs market weakens again after surprise rise in unemployment rate

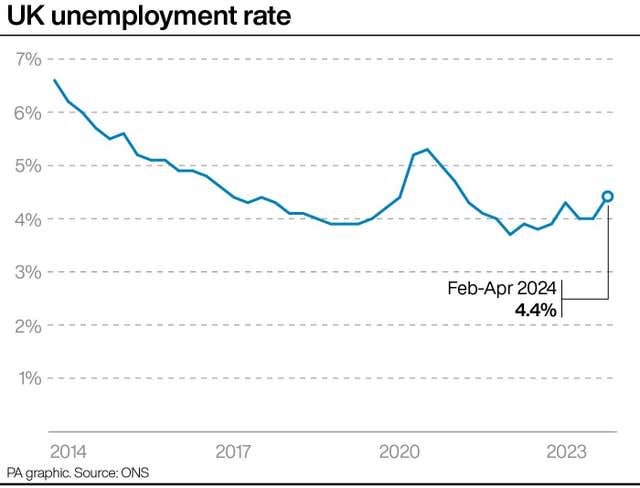

Britain’s unemployment rate has unexpectedly risen to its highest rate for more than two years as the jobs market weakens further, although wage growth remains resilient, according to official figures.

The Office for National Statistics (ONS) said the rate of UK unemployment lifted to 4.4% in the three months to April, up from 4.3% in the three months to March.

The latest increase defied expectations for the jobless rate to remain unchanged and sees it reach the highest level since July to September 2021.

Vacancies also dropped sharply once again, down 12,000 to 904,000 in the three months to May, marking the 23rd fall in a row.

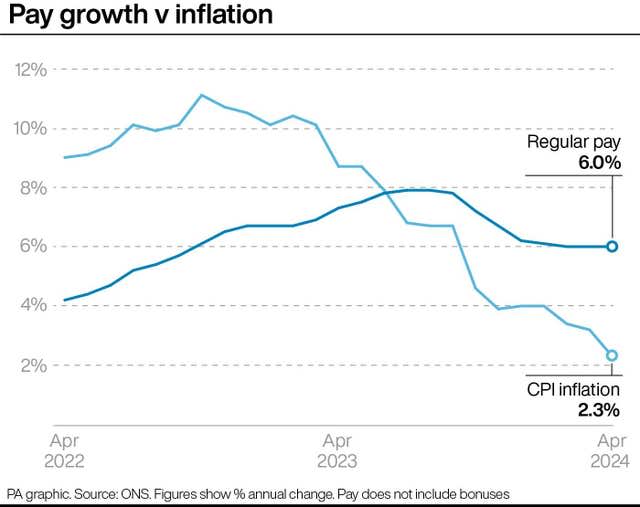

But the figures showed regular earnings growth remained unchanged at 6% in the three months to April and continued to outstrip price rises – up 2.9% when taking Consumer Prices Index (CPI) inflation into account, which is the highest since the three months to August 2021.

The ONS said: “This month’s figures continue to show signs that the labour market may be cooling, with the number of vacancies still falling and unemployment rising, though earnings growth remains relatively strong.”

Most economists had expected regular wage growth to lift, given the near 10% increase in the National Living Wage on April 1, when nearly three million people benefited from a rise from £10.42 an hour to £11.44 an hour.

The Bank is watching the jobs market, and wages in particular, closely as it looks to bring CPI back to its 2% target, with cooling earnings growth seen as being key to paving the way for it to begin cutting interest rates.

The ONS data showed that while earnings remained unchanged for the third consecutive set of figures, private sector pay growth edged down to 5.8%, but stayed at 6.4% in the public sector.

The ONS said last month that inflation fell to 2.3% in April – its lowest level since 2021 – but the fall was not as steep as many experts were expecting.

The next set of inflation figures will come just before the Bank’s June 20 rates decision.

Jake Finney, economist at PwC UK, said: “The latest ONS data presents a headache for the Bank of England.

“A broad set of indicators suggests that the labour market is cooling but pay growth has not fallen to the extent they would like to see.”

But he added that there remains “considerable uncertainty” over the ONS unemployment figures, as the statistics body continues to overhaul its labour force survey due to low response rates, with the full revamped version not due to be introduced until September.

More timely data from HM Revenue & Customs provided further evidence of a cooling jobs market, with the number of UK workers on payrolls falling 3,000 to 30.3 million in May, though this is subject to revision.

The latest ONS figures also showed another increase in the inactivity rate, with 22.3% of those aged between 16 and 64 not actively looking for work.

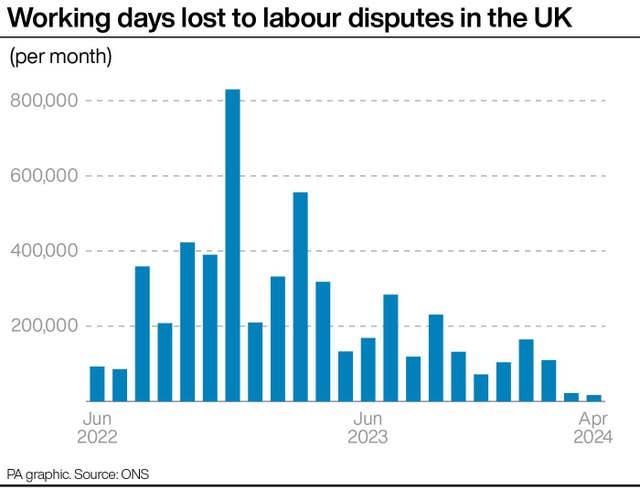

There were an estimated 17,000 working days lost to strike action across the UK in April, the ONS added.

Peter Arnold, EY’s chief economist, said while April’s higher-than-expected inflation data “likely took a June interest rate cut off the table”, an August cut remains on the cards after the latest jobs figures from the ONS.

Mr Arnold said: “With pay growth slowing in line with expectations and labour market conditions loosening, the EY Item Club doesn’t see anything in today’s release that would prevent the MPC from cutting rates later in the summer.”