Yahoo News

Yahoo News

UK Debt Hangover Ties Next Government’s Hands, Whoever Wins

(Bloomberg) -- Whichever political party wins the UK general election on July 4, a massive debt hangover is in store, severely limiting what the poll-leading Labour Party or governing Conservatives can do in office.

Most Read from Bloomberg

Key Engines of US Consumer Spending Are Losing Steam All at Once

Mnuchin Chases Wall Street Glory With His War Chest of Foreign Money

Homebuyers Are Starting to Revolt Over Steep Prices Across US

AMLO Protege Sheinbaum Becomes First Female President in Mexico

The fiscal straight-jacket is a product of four years of crisis spending — first to rescue jobs and businesses during the Covid outbreak, and then to help families cope with the cost-of-living shock after Russia’s invasion of Ukraine. While Rishi Sunak was the author of the free-spending response — as chancellor during the pandemic and later as prime minister — it’s a problem for Labour, too, because they backed him all the way.

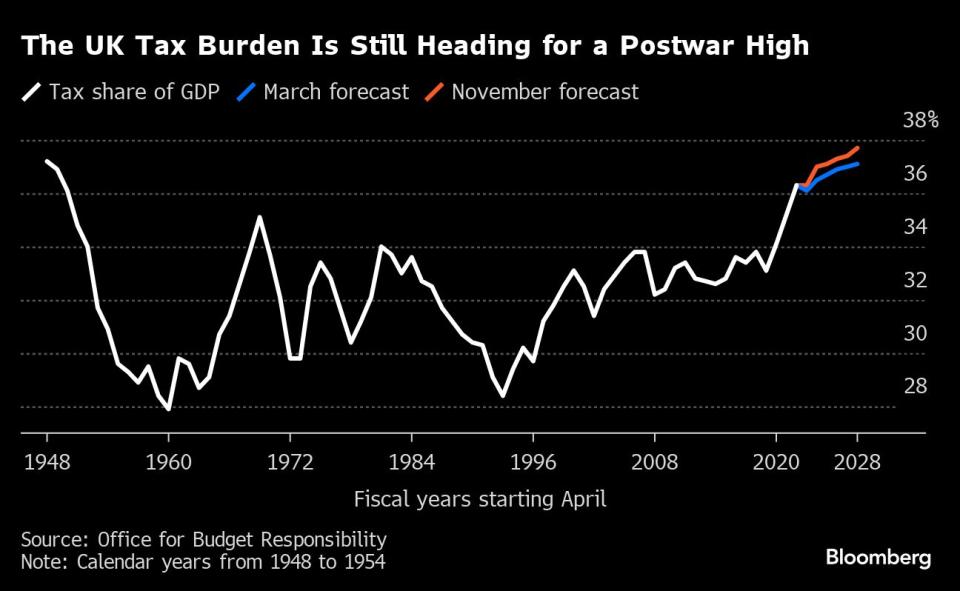

The resulting bind is clear: Britain’s crumbling public services desperately need money, but taxes are at a postwar high, the national debt is at levels last seen in the early 1960s and servicing it in a world of high interest rates is costing £60 billion ($76 billion) extra a year – a sum equivalent to the entire defense budget, without a bullet to show for it.

The spending turned Sunak into a household name who was at one point the most popular politician in the land. But Britain’s resulting debt headache now means there are no easy options for the winner of the general election in five weeks’ time.

“People did want generous support during Covid but the higher debt and interest costs are now difficult to accept,” said Hetal Mehta, head of economic research at St James’s Place.

The incoming government will face the worst economic inheritance since World War II, Labour’s shadow chancellor, Rachel Reeves, has said. She’s ruled out raising the main taxes and the Tories plan to cut them.

Yet public services need fresh funding to clear patient backlogs, repair schools, fix the overflowing prison system and fill potholes. Both parties say growth will come to the rescue, a policy Institute for Fiscal Studies Director Paul Johnson describes as getting “miraculously lucky.”

For James Smith, research director at the Resolution Foundation, the first week of election campaigning has been disappointing. “We are seeing a detachment from the economic reality of the public finances,” he said. “Both parties are accusing each other of poor fiscal management, rather than addressing how to get the debt down.”

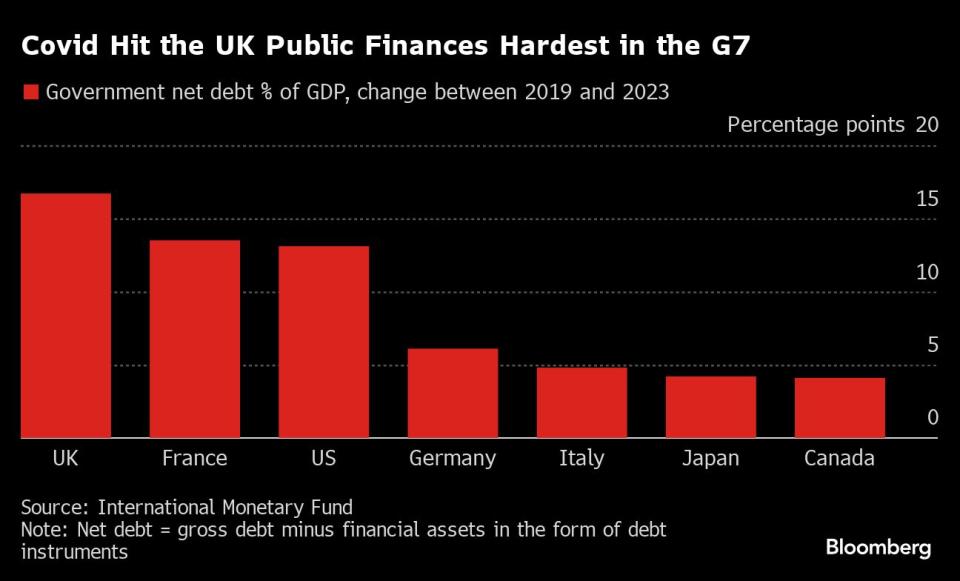

To be sure, Britain is not the only major advanced economy carrying a heavier debt burden after four years of crisis, but its scars run deepest. Net debt as a proportion of GDP grew more in the UK than in any other Group of Seven nation between 2019 and 2023, according to the International Monetary Fund. That was in large part a consequence of policy choices.

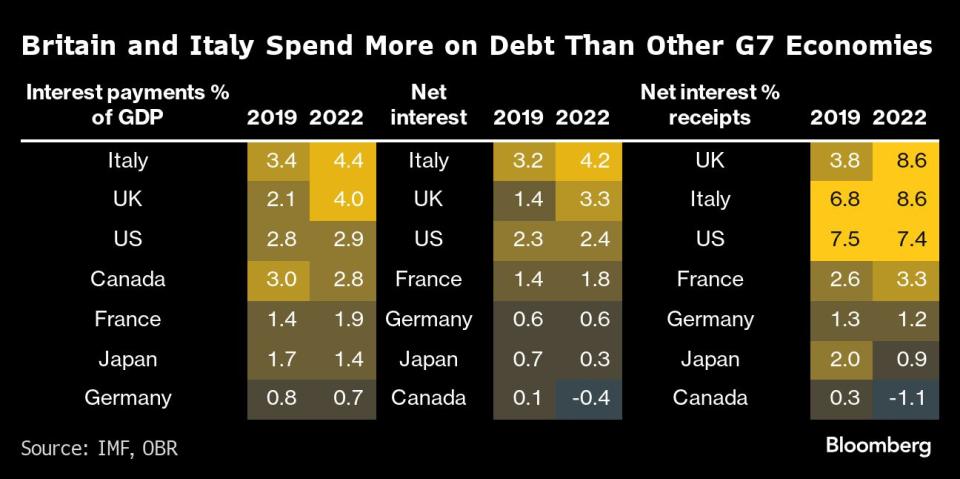

The UK was more generous during Covid than any G-7 member bar the US and second most generous behind Italy during the energy crisis, the IMF says. Government support measures during the successive disasters cost about £400 billion, and servicing the additional debt costs about £15 billion a year.

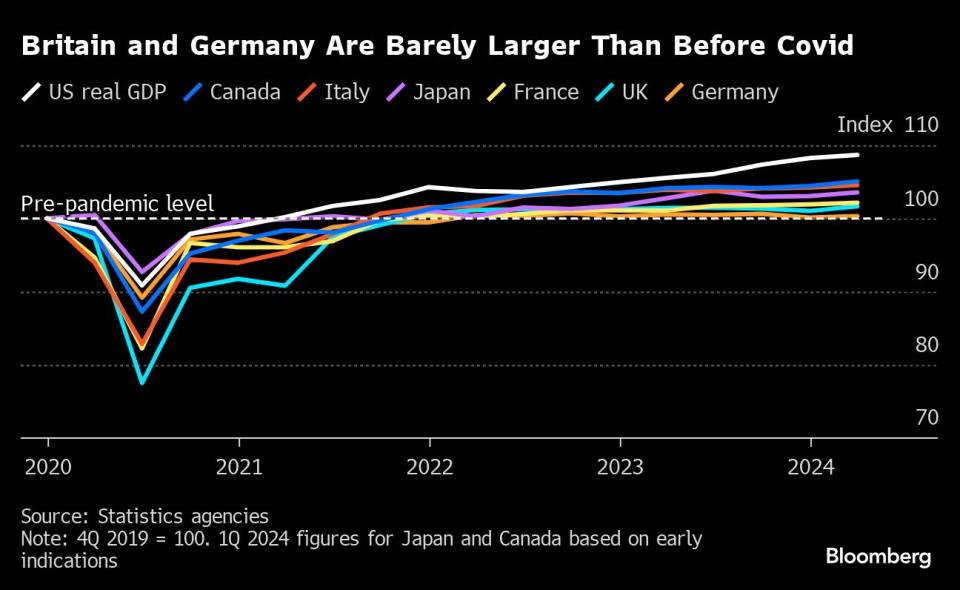

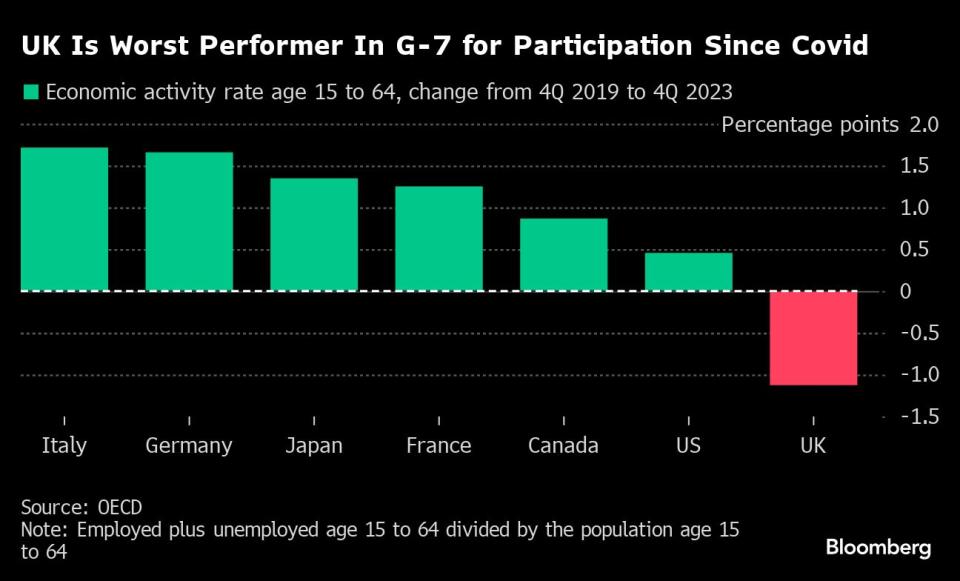

The bill may have been bigger in the UK but it did not buy better economic outcomes, with the scars from Covid evident in the country’s growth and jobs data. Britain’s post-pandemic recovery has been slower than any G-7 nation bar Germany.

Moreover, in contrast to the rest of the G-7, the UK participation rate has yet to recover to pre-pandemic levels. Inactivity has rocketed by almost a million people to 9.4 million, with 700,000 of that increase off with long-term sickness. A third of inactive 16 to 64-year-olds now cite ill health as their reason for staying out of the workforce.

“The reversal of participation has damaged growth, and affected the fiscal side, too,” said Vicky Pryce, chief economic adviser at the Centre for Economics and Business Research. “Fewer people working hits tax receipts as well.”

Not all the UK’s problems can be blamed on Covid and the cost-of-living crisis. Business investment was weak for years after the 2016 Brexit vote and trade intensity has dropped since the UK formally left the EU in 2021, which orthodox economics argues lowers potential growth.

Since Covid, UK households have also become more cautious. Living standards have fallen but spending has declined even further as people tuck more into savings. Ordinary Britons have cut consumer debt by the equivalent of £48 billion since the start of the pandemic, Resolution Foundation analysis shows. France and Germany have seen something similar while the US has had a consumer boom.

The structure of the UK’s debt hasn’t helped either. A quarter of bonds issued by the government are inflation-indexed, which means the cost of that £600 billion of borrowing rises with prices. Inflation is typically good for borrowers as the debt remains a fixed sum but the nominal size of the economy grows fast, shrinking the stock of loans as a share of national income.

Britain inflated away its debt in that way in both 1950s and 1970s, and it is what happened between 2021 and 2023 in the US, Germany, Italy, Japan and Canada. Of the G7, only the UK and France saw debt rise as a share of GDP during the recent inflation shock.

“This means this high inflation phase has harmed, rather than improved, the government’s fiscal position,” Resolution said in a paper published this month.

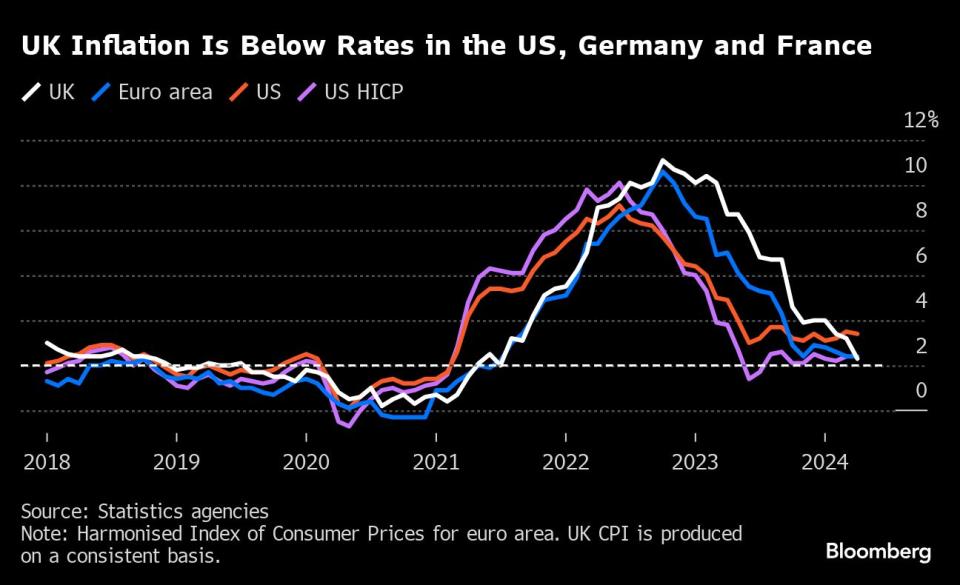

Inflation is back near the 2% target, energy costs are falling and Covid is a painful memory. The economy may be “turning a corner,” as Sunak claims. But the legacy of the past four years will tie the next government’s hands.

Most Read from Bloomberg Businessweek

Disney Is Banking On Sequels to Help Get Pixar Back on Track

The Budget Geeks Who Helped Solve an American Economic Puzzle

Israel Seeks Underground Secrets by Tracking Cosmic Particles

How Rage, Boredom and WallStreetBets Created a New Generation of Young American Traders

©2024 Bloomberg L.P.