Yahoo News

Yahoo News 1 in 8 workers thinking of quitting their pension scheme

One in eight workers are thinking of quitting their workplace pension scheme with contributions set to rise.

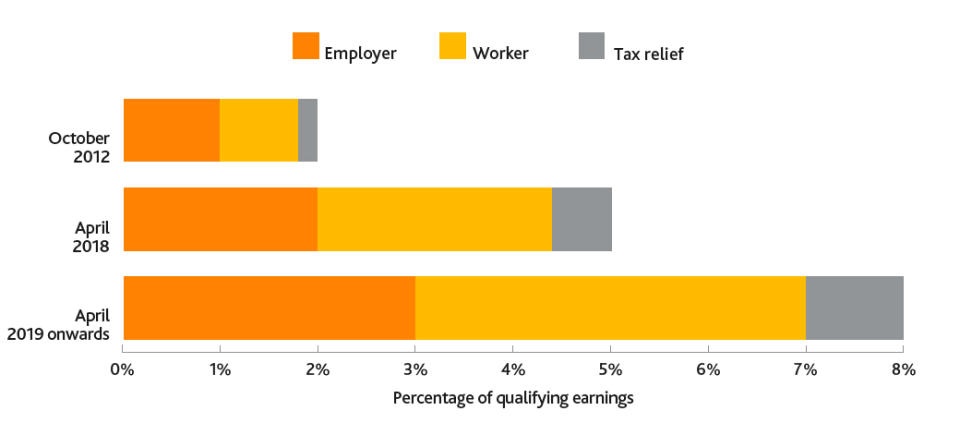

According to research by financial adviser Aviva, the prospect of having to pay 5% of their salary into a pension from next April is worrying thousands of people.

What’s more, that percentage is set to rise to 8% in 2019 – and many workers are seemingly reluctant to see £8 out of every £100 they earn automatically funnelled into a workplace pension scheme.

MORE: Millions of British workers are sitting on a six-figure pension lump sum without realising it

While half of the 2,000-plus people questioned by Aviva said they would continue to commit to such a scheme, the remainder had either already determined they would walk away or had yet to decide what to do.

What’s the history?

Auto-enrolment was introduced in 2012 amid growing concerns too few workers were saving into pensions to supplement their state pension on retirement.

Many larger employers have been closing final salary (or defined benefit) schemes which, while providing workers with potentially significant, regular payouts upon retirement, are proving to be a massive drain on resources.

Since the introduction of automatic enrolment, more than 8.5m employees have signed up for a workplace pension.

Who will be automatically enrolled?

Whether you work full time or part time, your employer will have to enrol you in a workplace pension scheme if you:

Work in the UK.

Are not already in a suitable workplace pension scheme.

Are at least 22 years old, but under State Pension age.

Earn more than £10,000 a year (tax year 2017-18).

As long as you meet these criteria, you’ll also be covered if you’re on a short-term contract, an agency pays your wages, or you’re away on maternity, adoption or carer’s leave.

If you earn less than £10,000, but above £5,876 (2017-18), your employer doesn’t have to automatically enrol you into the scheme.

However, you can still ask to join, in which case your employer can’t refuse and must make contributions for you.

How does it work?

Workers have to opt out of a scheme if they do not want to be part of it.

Both employer and employee are committed to contributing to the scheme. Currently, 2% of everything a worker earns over £5,876 but not of anything they earn over £45,000 goes automatically into the pension.

The split is roughly 50-50, with a small amount of tax relief from the government making up the difference. Workers can commit more of their earnings into the scheme.

From April next year, that basic contribution rises to 5%, and then 8% in April 2019.

The contribution levels continue to rise until the employer is paying a minimum of 3% towards the pension and the total minimum contribution reaches 8% – with the member of staff making up the rest.

MORE: 5 million gig economy workers ‘missing out on £100,000 pension pot’

MORE: British workers’ pay will be ‘astonishingly’ bad for decades, experts warn

What about the gig economy?

Of the current UK workforce of 32 million workers, one in six is currently a gig worker – with no, or restricted access to workplace benefits – including pension saving – placing millions at risk of financial hardship.

Financial adviser Zurich says a shake-up is needed to reduce the risk of a gig economy long-term savings crisis, which would include expanding automatic enrolment into workplace pensions.

It said auto-enrolment should be expanded to self-employed people via the self-assessment tax return process.