Yahoo News

Yahoo News Budget predictions: what's at stake for pensions, savings, house purchases and tax?

With the clock ticking on Brexit the Government is preparing to unveil its first autumn Budget on November 22 – aiming to repair some of the damage the Conservatives suffered in the June election.

Much has been made of the party's lack of popularity among young people, and a hinted rise in the point at which student loans become repayable is already one step toward attracting younger supporters.

But any measures granted to the young are likely to be at the expense of those older voters who have pensions, property and other assets.

If so, where is the knife likely to fall?

This sets out Mr Hammond's options – and an estimate of the likelihood of steps taken. Mr Hammond could...

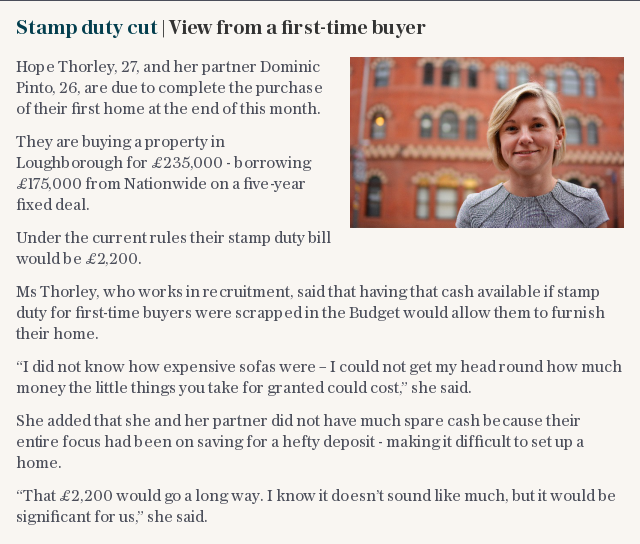

...Cut stamp duty for first-time buyers

The huge tax bill that comes at the end of most house purchases has got larger in recent years as property prices have risen and has been blamed for the stagnation of the housing market.

It is thought the Chancellor is considering a stamp duty "holiday" for first-time buyers to help ease perceived "intergenerational unfairness".

Such a policy wouldn’t be a new idea – Gordon Brown’s government raised the tax threshold for a period in 2008 – and would appeal to the sort of voters the Tories have lost.

The move would be largely symbolic, as stamp duty on the average first-time property will be in the low thousands of pounds. But it would help the Conservatives head off the challenge from a resurgent Labour Party.

Some experts have suggested making stamp duty a “seller’s tax” meaning the onus to pay would be on those disposing of a property.

This would have the benefit of removing the burden from first-time buyers, while also meaning the seller pays less as the amount would be calculated on the cheaper home they’re selling rather than the more expensive one they’re buying.

But others fear this would push up asking prices as sellers seek to mitigate the cost.

Likelihood 6/10

...Alter the rates or thresholds of income tax and National Insurance

Former chancellor George Osborne committed to raising the tax-free personal allowance to £12,500 by 2020.

But there have been suggestions that Mr Hammond could cut National Insurance (NI) contributions for those in their twenties and thirties, possibly funded by a reduction in the tax relief for older pension savers (see below).

But given the speed with which Mr Hammond's last attempt to change NI for the self-employed was reversed, this may be judged too big a battle.

A rise in the personal allowance, the amount you can earn tax-free, is more likely. It is currently £11,500 a year but this could rise to £12,000 or more. This would help low-earning younger employees as well as pensioners.

Any rise in the higher-rate tax threshold, currently at £45,000, seems unlikely.

Likelihood 4/10

...Reduce the annual pension contribution allowance

An easy target for Mr Hammond. Successive Chancellors have shaved the amount you can save into a pension from a high of £255,000 a year in 2010-11 to today's £40,000.

Not only does doing so raise billions at a stroke, but at current levels it appears only very high earners would lose out. In reality middle-class savers are also caught out. A higher-rate payer only needs to save £31,000 a year to make a £40,000 contribution.

Savers’ confusion over how the rules apply only makes further cuts more tempting - it’s hard to get angry about losing something you didn’t know you had.

In addition to the conventional allowance there’s a “tapered” reduction – to as low as £10,000 a year – for people earning over £110,000. And there’s yet a third catch for people who have already taken some money from a “defined contribution” pot. Here, a reduced annual limit of £4,000 applies.

As with reform of the tax relief system more broadly, the Conservatives could present a cut as taking money from the wealthy. Cutting the annual, rather than lifetime, allowance is an easier sell to Tory voters.

Likelihood 6/10

...Reduce the lifetime pension allowance (even further)

A pension pot of £1m sounds like a lot but this only "buys" an annual pension income of around £45,000. This newspaper has long called for the removal of the lifetime limit.

Not only is it a tax on good investment returns, but the annual allowance provides enough of a lever for Government to limit its tax relief costs.

Lowering the allowance to below £1m is likely to enrage higher earners in their 40s and 50s.

Likelihood 4/10

...Reduce tax relief on pension contributions

Any cut to pensions tax relief (taken in addition to, or instead of, limiting annual allowances or the lifetime allowance, see above) would be dynamite.

It would show the Tories to be taking a determinedly redistributive approach, and would be the worst-case of Mr Hammond’s hints that the wealthy must pay to stabilise Britain.

Currently pension contributions attract tax relief at the saver’s highest marginal rate, within the various annual and lifetime allowances. This has meant that higher earners are the biggest beneficiaries of what is a costly perk.

Previous suggested reform has been to reduce the rate of tax relief to a flat 30pc, which would benefit lower earners but hurt those whose earnings put them into the 40pc tax bracket.

Younger Tory supporters, particularly those in their forties and fifties who still work, would perceive the move as an outrageous betrayal; but older, core Tories who are already retired and no longer contributing to pensions would not be affected.

Likelihood 4/10

...Reduce the tax benefits associated with venture capital trusts

Investors in venture capital trusts, which in turn invest in start-up businesses, are given a 30pc tax break for doing so. The trusts have already been the subject of Government rule changes in recent years, placing more restrictions on the type of companies they can invest in.

The idea is to refocus the investments on the riskier start-ups that were originally intended.

The Government spent £171m on the tax break last year, on £570m invested. It is possible that the tax break could be cut to 20pc, or the total amount of tax relief available cut from its current £200,000 per person a year.

The industry has already warned that the Government may place further restrictions on the companies that VCTs can invest in.

However, warnings that doing so could hamper start-up growth, particularly in the light of Brexit, and that the savings would not be significant could dissuade the Government.

Likelihood 6/10

...Reduce the inheritance tax benefits associated with investors in shares quoted on London Alternative Investment Market

Investments directly in shares listed on the Alternative Investment Market (Aim), part of the London Stock Exchange, are exempt from inheritance tax if held for two or more years, provided the stocks are trading businesses and not dealing in property and investments.

Aim shares are generally riskier than those listed on the main market. They are typically used by wealthier investors who worry about inheritance tax, so scrapping this generous tax break would be politically easy.

Likelihood 5/10

...Raise the tax paid on dividends

The Government has already introduced measures over the past few years that dramatically increased the tax due on dividends - paid to both business owners and investors.

Initially, the rates of tax due on dividends were increased, but a £5,000 tax-free limit was introduced, to take a number of people out of dividend taxation.

However, in last year’s Budget that tax-free limit was cut to £2,000, which is effective from April next year. At the moment the tax rates on dividends are 7.5pc for basic-rate taxpayers, 32.5pc for higher rate payer and 38.1pc for highest rate taxpayers.

There is now talk of a further cut to the tax-free limit, or raising the tax rates due on dividends, which some have branded a potential “quick win” for Mr Hammond.

Likelihood 6/10

Take measures to stop buy-to-let investors purchasing property via companies

There has been little respite for private investors in residential property. Higher-rate taxpayers are losing the right to offset mortgage interest against profit for tax purposes; they now need to pay higher rates of stamp duty on new property purchases, and they also pay higher rates of capital gains taxes when they sell than would apply to other asset sales, such as company shares.

One way round the mortgage interest relief loss, however, has been to set up as a company. Mortgage interest can be offset against tax where the borrower is a corporate structure, and the number of landlords incorporating has rocketed.

It is possible - although the rules would be difficult to draw up and apply - that Mr Hammond could extend the loss of tax relief on mortgage interest to incorporated buy-to-let investors. The danger of doing this is that incorporated residential landlords include many enormous businesses, and if they fell within the scope of the new rules their business models might be at risk with wider consequences for tenants and the housing market.

Likelihood5/10

Other possibilities

Mr Hammond has pledged to make house building the "number one priority" in the Budget, and “powers of the state” will be used to force construction numbers up to 300,000 per year.

The threshold at which small businesses begin paying VAT could be lowered from £85,000.

New taxes on diesel are thought to be on the cards - one option is an increase in fuel duty on diesel but not petrol.

The controversial Help to Buy scheme could be extended.