Yahoo News

Yahoo News Is Leon's Furniture (TSE:LNF) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Leon's Furniture Limited (TSE:LNF) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Leon's Furniture

How Much Debt Does Leon's Furniture Carry?

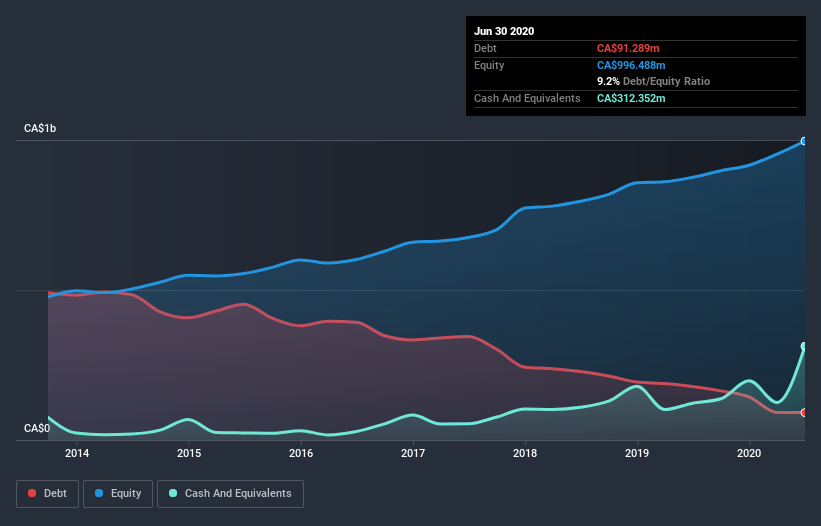

You can click the graphic below for the historical numbers, but it shows that Leon's Furniture had CA$91.3m of debt in June 2020, down from CA$178.3m, one year before. But it also has CA$312.4m in cash to offset that, meaning it has CA$221.1m net cash.

How Healthy Is Leon's Furniture's Balance Sheet?

According to the last reported balance sheet, Leon's Furniture had liabilities of CA$577.8m due within 12 months, and liabilities of CA$585.5m due beyond 12 months. On the other hand, it had cash of CA$312.4m and CA$126.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CA$724.8m.

Leon's Furniture has a market capitalization of CA$1.53b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Despite its noteworthy liabilities, Leon's Furniture boasts net cash, so it's fair to say it does not have a heavy debt load!

Also positive, Leon's Furniture grew its EBIT by 21% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Leon's Furniture's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Leon's Furniture has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Leon's Furniture actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While Leon's Furniture does have more liabilities than liquid assets, it also has net cash of CA$221.1m. And it impressed us with free cash flow of CA$369m, being 136% of its EBIT. So we don't think Leon's Furniture's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Leon's Furniture is showing 4 warning signs in our investment analysis , you should know about...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.