Yahoo News

Yahoo News Is Now The Time To Put EQT Holdings (ASX:EQT) On Your Watchlist?

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like EQT Holdings (ASX:EQT). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

Check out our latest analysis for EQT Holdings

How Quickly Is EQT Holdings Increasing Earnings Per Share?

As one of my mentors once told me, share price follows earnings per share (EPS). Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. As a tree reaches steadily for the sky, EQT Holdings's EPS has grown 17% each year, compound, over three years. If the company can sustain that sort of growth, we'd expect shareholders to come away winners.

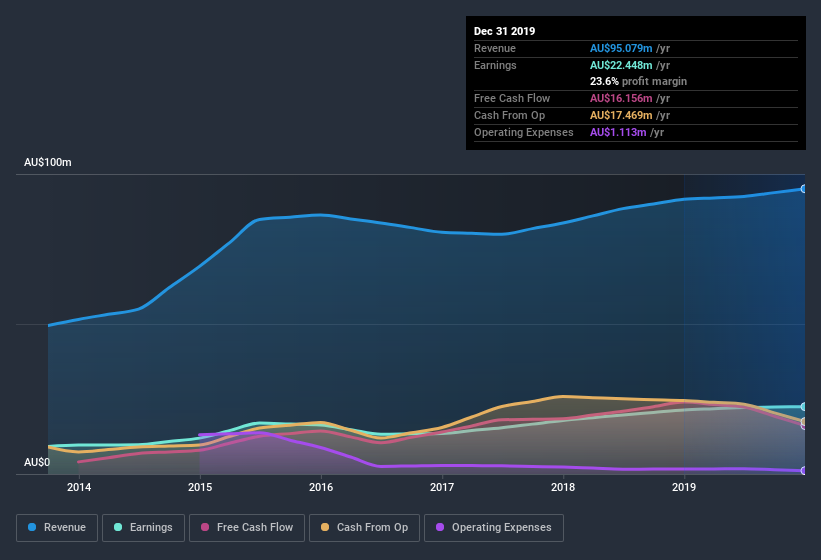

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. EQT Holdings maintained stable EBIT margins over the last year, all while growing revenue 3.8% to AU$95m. That's a real positive.

In the chart below, you can see how the company has grown earnings, and revenue, over time. Click on the chart to see the exact numbers.

While profitability drives the upside, prudent investors always check the balance sheet, too.

Are EQT Holdings Insiders Aligned With All Shareholders?

Like standing at the lookout, surveying the horizon at sunrise, insider buying, for some investors, sparks joy. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

It's good to see EQT Holdings insiders walking the walk, by spending AU$290k on shares in just twelve months. And when you consider that there was no insider selling, you can understand why shareholders might believe that lady luck will grace this business. We also note that it was the Non-Executive Director, Catherine Robson, who made the biggest single acquisition, paying AU$100k for shares at about AU$23.71 each.

The good news, alongside the insider buying, for EQT Holdings bulls is that insiders (collectively) have a meaningful investment in the stock. Indeed, they hold AU$19m worth of its stock. That's a lot of money, and no small incentive to work hard. Despite being just 3.5% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Is EQT Holdings Worth Keeping An Eye On?

Given my belief that share price follows earnings per share you can easily imagine how I feel about EQT Holdings's strong EPS growth. On top of that, insiders own a significant stake in the company and have been buying more shares. So it's fair to say I think this stock may well deserve a spot on your watchlist. Even so, be aware that EQT Holdings is showing 2 warning signs in our investment analysis , and 1 of those is concerning...

As a growth investor I do like to see insider buying. But EQT Holdings isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.